Consumers around the world are displaying a growing preference for global brands rather than locally manufactured products, according to a new study by performance management company Nielsen.

Consumers around the world are displaying a growing preference for global brands rather than locally manufactured products, according to a new study by performance management company Nielsen.

The annual Nielsen Global Brand-Origin Report highlights consumers’ preference for and sentiment toward products manufactured by local manufacturers versus large global/multinational brands across 34 categories. While the survey findings have pointed to a relatively balanced view across global and local brands in recent years, the latest results show consumer preference is tipping toward global brands across the majority of categories.

Preference for global brands was strongest in the baby wipes/diapers and baby food/formula categories, where just 7% and 10% of consumers, respectively, said they prefer to buy brands from local manufacturers. Other categories where consumers showed low preference for local brands include vitamins/supplements (12% prefer local), pet food (12%), feminine care products (13%), energy drinks/sports drinks (14%), and canned/tinned food products (15%).

Conversely, categories where consumers were more inclined to opt for a locally manufactured product over a global brand included dairy products (54%), biscuits/chips/snacks/cookies (32%), ice-cream (31%) and mineral/bottled water (30%).

Categories that saw the most notable swing in preference away from local brands compared to the previous survey conducted in 2015 include mineral/bottled water (down 22 percentage pts [pps] to 30%), instant noodles (down 21 pps to 21%), oral care products (down 15 pps to 18%), laundry products (down 13 pps to 21%), pet foods (down 13 pps to 12%), carbonated soft drinks (down 12 pps to 18%) and baby wipes/diapers (down 11 pps to 7%). The hair care (18%), alcohol (16%) and baby food/formula (10%) categories all saw a 10-pp decline in preference for local brands from 2015.

Categories that saw the most notable swing in preference away from local brands compared to the previous survey conducted in 2015 include mineral/bottled water (down 22 percentage pts [pps] to 30%), instant noodles (down 21 pps to 21%), oral care products (down 15 pps to 18%), laundry products (down 13 pps to 21%), pet foods (down 13 pps to 12%), carbonated soft drinks (down 12 pps to 18%) and baby wipes/diapers (down 11 pps to 7%). The hair care (18%), alcohol (16%) and baby food/formula (10%) categories all saw a 10-pp decline in preference for local brands from 2015.

“In today’s world of hyper-connectivity and globalization, consumers have a wider array of product choices than ever before,” observes Regan Leggett, Head of Foresight and Thought Leadership, Growth Markets, Nielsen.

“Importantly, consumers also have greater access to global brands than they have in the past, thanks to factors such as expanding distribution, e-commerce offerings, and modern trade retail channels. As a result, we’re seeing a swing in preference toward the big multinationals. Other factors at play include consumer perception around quality, particularly in high involvement categories such as baby care.”

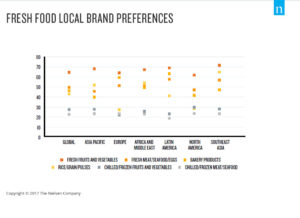

At a regional level, market nuances were evident, with consumer preference for global versus local brands varying widely within a number of categories. In the dairy category, consumer preference for local brands was much more pronounced in Africa and the Middle East (73%) and Europe (66%) compared to the global average (54%).

In the biscuits/chips/snacks/cookies category, consumer preference for local brands was prevalent in Southeast Asia (50%), Africa and the Middle East (41%) and Latin America (41%) compared to 32% globally. In Europe, consumers were much more likely to opt for local alcohol brands compared to the global average (22% vs. 16%), while Southeast Asian consumers showed stronger affinity for local instant noodle brands compared to the global average (39% vs. 21%).

“The variation across regions illustrates the relative strength of local manufacturers within specific categories, particularly where they are appealing to local consumers’ tastes,” emphasizes Leggett.

“The variation across regions illustrates the relative strength of local manufacturers within specific categories, particularly where they are appealing to local consumers’ tastes,” emphasizes Leggett.

“In Southeast Asia, for example, where noodles are a staple in consumers’ diets, local manufacturers have been able to maintain a stronghold on the category. Similarly in European markets locally sourced dairy products are perceived to be of a higher quality than imported products.”

Leggett concluded: “In an increasingly global world, the battle of the brands comes down to understand consumers’ evolving needs, behaviors, lifestyles and tastes. Any brand, be it local or global, that is able to tap into these consumer preferences will be best-placed to win the hearts and minds of consumers in the future.”

Source: Nielsen

Global brands are winning the battle for consumers’ hearts and minds, according to Nielsen added by newsroom on

View all posts by newsroom →

You must be logged in to post a comment Login